*Colin Livingston

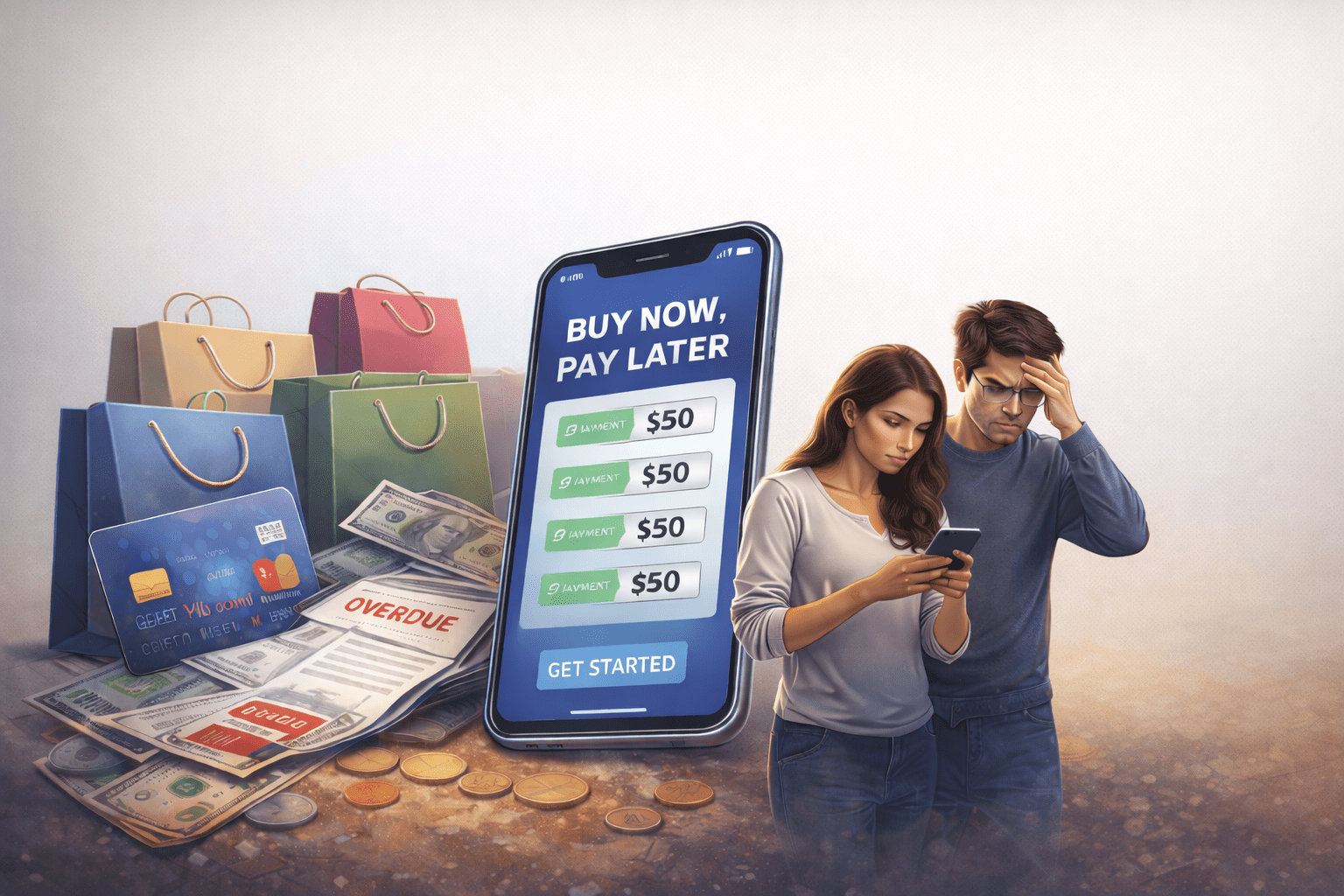

I. Introduction

“Buy now, pay later” programs have quickly become a popular interest-free credit option, with disproportionately high use “among financially vulnerable consumers.”[1] Retailers offer these programs “through payment platforms like Afterpay, Klarna, and Affirm[,]” allowing consumers to pay for “online or in-store purchases. . . [through] installments over a short period” of time.[2] According to a 2025 survey, about one in three U.S. adults has used a “buy now, pay later” service for at least one purchase.[3] Furthermore, the global “buy now, pay later” (BNPL) market is projected “to reach $560.1 billion in 2025. . . [and] expand. . . to approximately $911.8 billion” by the end of 2030, reflecting its rapid growth in how consumers finance and purchase products.[4] Despite the development of this credit option, BNPL programs are not subject to the same regulatory requirements governing traditional credit card companies, including Regulation Z, which implements the Truth in Lending Act.[5]

II. Consumer Vulnerability and Financial Risk in BNPL Lending

Debt related to traditional credit card purchases is already a serious problem for many Americans,[6] and BNPL programs only add to this issue.[7] Those who use these programs tend to be in financially vulnerable positions, with lower credit scores and a greater incidence of thirty-day delinquencies on other loans.[8] Moreover, these consumers are more likely to be denied traditional credit, carry revolving balances on their credit cards, and hold higher levels of debt with “fewer liquid assets.”[9] To make matters worse, BNPL loan “providers [do not] run. . . hard credit check[s],” making these loans more attractive to those with limited or poor credit history.[10]

The structure of these programs makes consumers vulnerable to overextending their credit by “loan stacking and sustained usage.”[11] Those using BNPL lenders are likely to spend more on purchases than they would have without BNPL credit.[12] As a result, a borrower may take on multiple BNPL loans from different providers simultaneously, increasing the risk of repayment failure.[13] Furthermore, sustained usage of these lenders may risk “borrowers’ ability to meet non-BNPL financial obligations such as rent,. . . mortgages, or auto loans.”[14] Although marketed as an interest-free credit option,[15] borrowers also risk accumulating “hidden interest.”[16] This cost may arise in the form of late fees for missed payments or by accruing revolving interest if they use a credit card to make an installment payment, negating many of the supposed benefits of interest-free credit.[17]

Although BNPL programs operate as a new form of credit, they remain outside the regulatory framework governing traditional credit cards.[18] In the absence of consumer protection restrictions, BNPL lenders can exploit regulatory gaps that could leave already vulnerable consumers in an even worse financial position.[19]

III. Regulatory Failures and the Limits of the TILA

Congress sought to protect consumers from the risks inherent in credit markets through the Truth in Lending Act (TILA).[20] TILA is designed to protect consumers by requiring clear, standardized “disclosure of credit terms, enabling borrowers to compare” offers across financial institutions and make informed credit decisions.[21] The Consumer Financial Protection Bureau (CFPB) created Regulation Z to implement TILA.[22] However, BNPL lending has exposed new shortcomings in this decades-old framework.[23] In May 2024, the CFPB issued an interpretive rule under Regulation Z determining that digital credit accounts offered by BNPL lenders are subject to some of the same consumer protection requirements under TILA that govern traditional credit options.[24]

The CFPB’s interpretive rule faced immediate scrutiny when the Financial Technology Association (FTA) filed suit against the Bureau in October 2024.[25] The FTA argued that the rule bypassed “key procedural and substantive requirements of the Administrative Procedure Act” and that BNPL services do not fall within the lending categories covered by TILA.[26] As a result of the FTA’s challenges, the CFPB and FTA agreed in March to stay the case while the Bureau worked to revoke its interpretive rule on BNPL programs.[27] During the stay, the CFPB was required to provide status reports on its progress to the court every thirty days.[28] In its final status report before the FTA filed a stipulation of dismissal, the CFPB agreed with many of the FTA’s arguments and stated that it “does not intend to issue a revised rule” concerning BNPL lenders.[29] Ultimately, the CFPB’s first attempt at regulating BNPL lenders failed to withstand legal challenge, and its interpretive ruling was revoked.[30]

The revocation of this interpretative rule falls in line with a “series of regulations and lawsuit defenses the agency has abandoned as the [Bureau’s new] director, Russel Vought, seeks to shrink the [CFPB]. . . and reverse [actions of the] Biden administration.”[31] Consequently, BNPL programs will continue to operate in a largely unregulated space.[32] The CFPB effectively leaves consumers using BNPL lenders without standardized disclosure requirements, dispute-resolution mechanisms, and a plethora of other protections afforded to those who use traditional credit cards.[33] Consumers using BNPL credit will continue to struggle with these “operational hurdles,” and BNPL lenders will continue to take advantage of those who are most vulnerable.[34]

IV. Conclusion

BNLP programs have grown rapidly, with many consumers taking advantage of a new short-term interest-free credit option.[35] These programs, however, have raised concerns that their users are typically in financially vulnerable positions and risk overextending their credit.[36] With the CFPB’s attempt to regulate BNPL lenders failing, new regulations will be needed to protect consumers from the risks associated with BNPL credit.[37]

*Colin Livingston is a second-year student at the University of Baltimore School of Law where he is a Staff Editor for Law Review and a Distinguished Scholar of the Royal Graham Shannonhouse III Honor Society. Prior to law school, Colin earned a Bachelor of Arts in Government and Politics from the University of Maryland, College Park. Next summer he will be working as a Law Clerk for Eccleston & Wolf.

[1] Joanna Stavins, Buy Now, Pay Later: Who Uses It and Why, Fed. Rsrv. Bank of Bos.: Current Policy Perspectives (May 23, 2024), https://www.bostonfed.org/publications/current-policy-perspectives/2024/buy-now-pay-later-who-uses-it-why.

[2] Id. (“typically four installments over six weeks.”).

[3] Lauren Nowacki, Survey: About Half of Buy Now, Pay Later Users Have Experienced Issues like Overspending and Missing Payments, Bankrate (May 5, 2025), https://www.bankrate.com/loans/personal-loans/buy-now-pay-later-survey/.

[4] Globe Newswire, Buy Now Pay Later Global Business Report 2025: BNPL Payments to Grow by 13.7% to Surpass $560 Billion this Year, Driven by Klarna, Afterpay, PayPal, and Affirm – Forecast to 2030, FINTECH FUTURES (Feb. 24, 2025), https://www.fintechfutures.com/press-releases/buy-now-pay-later-global-business-report-2025-bnpl-payments-to-grow-by-13-7-to-surpass-560-billion-this-year-driven-by-klarna-afterpay-paypal-and-affirm-forecast-to-2030.

[5] See John L. Culhane, Jr. & John D. Socknat, CFPB Will Not Issue Revised BNPL Rule, Ballard Spahr LLP: Consumer Finance Monitor (June 20, 2025), https://www.consumerfinancemonitor.com/2025/06/20/cfpb-will-not-issue-revised-bnpl-rule/; see infra Part III.

[6] Jessica Dickler, Credit Card Debt Reaches $1.21 Trillion — In Line With Last Year’s All-Time High, NY Fed Finds, CNBC (Aug. 5, 2025, at 14:49 ET), https://www.cnbc.com/2025/08/05/ny-fed-credit-card-debt-second-quarter-2025.html (showing that Americans collectively hold $1.21 trillion in credit card debt, a number that is growing alongside rising credit card delinquency rates).

[7] See infra text accompanying notes 11–17.

[8] Stavins, supra note 1, at 3; Felix Aidala, Daniel Mangrum & Wilbert van der Klaauw, Who Uses “Buy Now, Pay Later”?, FED. RSRV. BANK of N.Y. (Sep. 26, 2023), https://libertystreeteconomics.newyorkfed.org/2023/09/who-uses-buy-now-pay-later/.

[9] Stavins, supra note 1; Aidala, Mangrum & van der Klaauw, supra note 8.

[10] Maya Benjamin, What Is Buy Now, Pay Later?, CNBC SELECT (Aug. 8, 2025), https://www.cnbc.com/select/buy-now-pay-later-what-is-it/.

[11] Consumer Fin. Prot. Bureau, Buy Now, Pay Later: Market Trends and Consumer Impacts 64–69 (2022), https://files.consumerfinance.gov/f/documents/cfpb_buy-now-pay-later-market-trends-consumer-impacts_report_2022-09.pdf.

[12] See Dionysius Ang & Stijn Maesen, Research: How “Buy Now, Pay Later” Is Changing Consumer Spending, HARV. BUS. REV. (Nov. 26, 2024), https://hbr.org/2024/11/research-how-buy-now-pay-later-is-changing-consumer-spending.

[13] Consumer Fin. Prot. Bureau, supra note 11, at 65–66.

[14] Id. at 66.

[15] Id. at 3, 6.

[16] Id. at 22.

[17] Id. at 21–23 (exhibiting that 10.1% of consumers making purchases with BNPL programs used a credit card to make an installment payment in 2021); Matt Schulz, BNPL Tracker: 41% of Users Late in Past Year, More Using Loans for Groceries, lendingtree (Dec. 19, 2025), https://www.lendingtree.com/personal/buy-now-pay-later-loan-statistics/ (showing that 54% of users who responded to the survey have been “late on a BNPL loan in the past”).

[18] See discussion infra Part III.

[19] See infra text accompanying notes 31–34; supra text accompanying notes 6–17.

[20] Truth in Lending Act § 102, 15 U.S.C. § 1601; Nat’l Credit Union Admin., Federal Consumer Financial Protection Guide: Truth in Lending Act (Regulation Z) (2025), https://ncua.gov/regulation-supervision/manuals-guides/federal-consumer-financial-protection-guide/compliance-management/lending-regulations/truth-lending-act-regulation-z.

[21] See sources cited supra note 20.

[22] Regulation Z, 12 C.F.R. § 1026 (2024); Nat’l Credit Union Admin., supra note 20 (explaining that the TILA is implemented through Regulation Z by the CFPB).

[23] See infra text accompanying notes 25–30.

[24] Regulation Z, 12 C.F.R. § 1026 (2024) (concluding that BNPL providers operate as both “creditors” and “card issuers”).

[25] Complaint, Fin. Tech. Ass’n v. CFPB, No. 1:24-cv-2966 (D.D.C. Oct. 18, 2024).

[26] Id. at 1–3.

[27] John L. Culhane, Jr. & Joseph J. Schuster, CFPB Plans to Revoke BNPL Interpretive Rule, Ballard Spahr LLP: Consumer Finance Monitor (Mar. 28, 2025), https://www.consumerfinancemonitor.com/2025/03/28/cfpb-plans-to-revoke-bnpl-interpretive-rule/; Status Report and Joint Motion to Stay, Fin. Tech. Ass’n v. CFPB, No. 1:24-cv-2966 (D.D.C. Mar. 26, 2025).

[28] See sources cited supra note 27.

[29] John L. Culhane, Jr. & John D. Socknat, CFPB Will Not Issue Revised BNPL Rule, Ballard Spahr LLP: Consumer Finance Monitor (June 20, 2025), https://www.consumerfinancemonitor.com/2025/06/20/cfpb-will-not-issue-revised-bnpl-rule/; Status Report, Fin. Tech. Ass’n v. CFPB, No. 1:24-cv-2966 (D.D.C. June 2, 2025).

[30] See Culhane, Jr. & Socknat, supra note5; supra text accompanying notes 24–28.

[31] Justin Bachman, CFPB Plans to Spike BNPL Rule, PAYMENTS DIVE (Mar. 31, 2025), https://www.paymentsdive.com/news/cfpb-plans-to-spike-bnpl-rule/743933/.

[32] See Culhane, Jr. & Socknat, supra note 5.

[33] Id. (“These Regulation Z requirements included account-opening disclosures, billing statements, change in terms disclosure, payment processing, treatment of credit balances, issuance of cards, liability for unauthorized use, merchant disputes, billing disputes, crediting of returns, advertising . . . .”); see also Regulation Z, 12 C.F.R. § 1026 (2024) (implementing TILA regulations).

[34] Consumer Fin. Prot. Bureau, supra note 11, at 4; see discussion supra Part II.

[35] See discussion supra Part I; Consumer Fin. Prot. Bureau, supra note 11, at 3, 6.

[36] See discussion supra Part II.

[37] See discussion supra Part III.