*Colin Livingston

I. Introduction

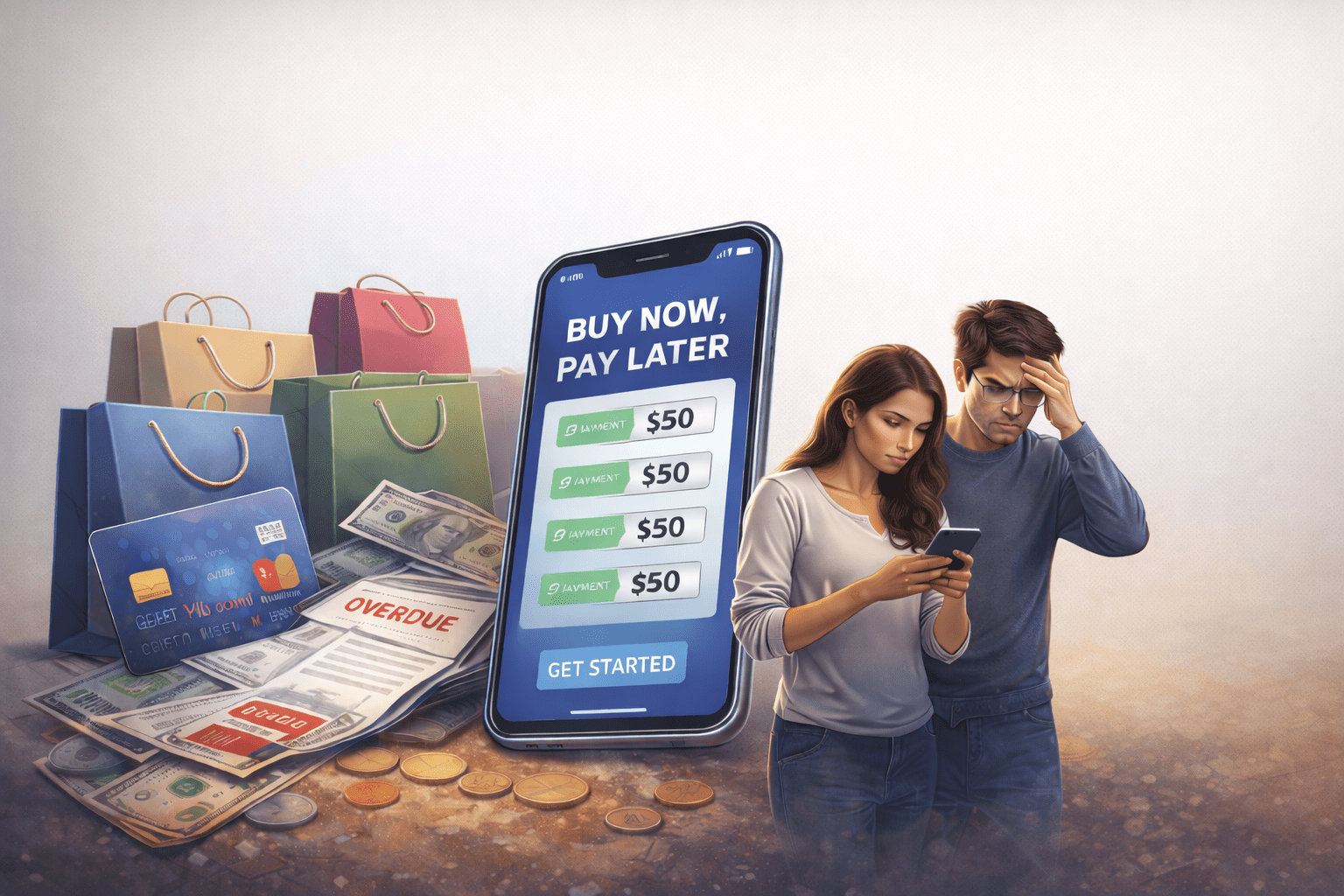

“Buy now, pay later” programs have quickly become a popular interest-free credit option, with disproportionately high use “among financially vulnerable consumers.”[1] Retailers offer these programs “through payment platforms like Afterpay, Klarna, and Affirm[,]” allowing consumers to pay for “online or in-store purchases. . . [through] installments over a short period” of time.[2] According to a 2025 survey, about one in three U.S. adults has used a “buy now, pay later” service for at least one purchase.[3] Furthermore, the global “buy now, pay later” (BNPL) market is projected “to reach $560.1 billion in 2025. . . [and] expand. . . to approximately $911.8 billion” by the end of 2030, reflecting its rapid growth in how consumers finance and purchase products.[4] Despite the development of this credit option, BNPL programs are not subject to the same regulatory requirements governing traditional credit card companies, including Regulation Z, which implements the Truth in Lending Act.[5]

Continue reading “Buy Now, Pay Later, Regulate Never: The CFPB’s Failed Attempt to Govern BNPL Lending”